DANL 210 - Unifying ESG Metrics with Financial Analysis

Author

Hayden Mikula

Published

May 15, 2025

In 2016, Morningstar released the first iteration of the Environmental, Social, and Governance (ESG) scores using data collected by Sustainalytic’s ESG research efforts, with the intention to make insider information surrounding companies and investment risk much more accessible to the public. Today these ratings are largely standardized, being featured alongside company’s financial information on prominent market data websites such as Yahoo Finance.

For these websites, the ESG ratings are indicators of an institution’s risk relating to various sustainability metrics and general level of public controversy, and serve as general influences to consumer investment. In a survey conducted by Morningstar in September of 2024, 67% of asset owners believe that the ESG rating scheme has become more integral to their investment decisions.

With these ratings being presented alongside company-wise financial data such as historical stock price and income statements, the question arises: Just how effective is the ESG rating in predicting public investment decisions / outlooks?

Exploratory Questions:

How concerned are companies with reducing their ESG risk?

Which industries typically have the highest ESG risk assessments?

Do ESG ratings affect stock prices?

Library & File Setup

import pandas as pdimport seaborn as snsimport matplotlib.pyplot as pltimport randomfrom google.colab import drivedrive.mount('/content/drive')

Drive already mounted at /content/drive; to attempt to forcibly remount, call drive.mount("/content/drive", force_remount=True).

The individual Total ESG, Environmental, Social, Governance, and Controversy ratings for 625 companies in 2024, along with the stock price financial data for these 625 companies from January 1st, 2024 - March 31st, 2025

The individual Total ESG, Environmental, Social, Governance, and Controversy ratings for 3135 companies in 2025

All data was scraped from each company’s Historical Data and Sustainability sections on Yahoo Finance respectively

ESG Data

esg_2024

Year

Symbol

Name

Sector

Industry

Country

Market_Cap

IPO_Year

total_esg

Environmental

Social

Governance

Controversy

0

2024

A

Agilent Technologies Inc. Common Stock

Industrials

Biotechnology: Laboratory Analytical Instruments

United States

40365434818

1999.0

13.6

1.1

6.4

6.1

2.0

1

2024

AA

Alcoa Corporation Common Stock

Industrials

Aluminum

United States

6622135551

2016.0

24.0

13.8

5.9

4.3

3.0

2

2024

AAL

American Airlines Group Inc. Common Stock

Consumer Discretionary

Air Freight/Delivery Services

United States

9088024606

NaN

26.4

9.9

11.6

4.8

2.0

3

2024

AAP

Advance Auto Parts Inc.

Consumer Discretionary

Auto & Home Supply Stores

United States

4474665296

NaN

11.5

0.1

8.3

3.1

2.0

4

2024

AAPL

Apple Inc. Common Stock

Technology

Computer Manufacturing

United States

2614310000000

1980.0

17.2

0.5

7.4

9.4

3.0

...

...

...

...

...

...

...

...

...

...

...

...

...

...

620

2024

XYL

Xylem Inc. Common Stock New

Industrials

Fluid Controls

United States

32010402681

2011.0

18.1

4.3

8.7

5.2

1.0

621

2024

YUM

Yum! Brands Inc.

Consumer Discretionary

Restaurants

United States

39885044416

NaN

20.1

4.5

11.4

4.1

2.0

622

2024

Z

Zillow Group Inc. Class C Capital Stock

Consumer Discretionary

Business Services

United States

10195469129

NaN

22.2

1.2

11.5

9.5

2.0

623

2024

ZBH

Zimmer Biomet Holdings Inc. Common Stock

Health Care

Industrial Specialties

United States

24476778026

NaN

26.0

3.6

14.5

7.9

2.0

624

2024

ZTS

Zoetis Inc. Class A Common Stock

Health Care

Biotechnology: Pharmaceutical Preparations

United States

72535308358

2013.0

18.8

3.2

6.8

8.7

2.0

625 rows × 13 columns

esg_2025

Year

Symbol

Name

Sector

Industry

Country

Market_Cap

IPO_Year

total_esg

Environmental

Social

Governance

Controversy

0

2025

A

Agilent Technologies Inc. Common Stock

Industrials

Biotechnology: Laboratory Analytical Instruments

United States

3.391867e+10

1999.0

10.1

1.1

5.0

3.9

1.0

1

2025

AA

Alcoa Corporation Common Stock

Industrials

Aluminum

United States

8.279121e+09

2016.0

25.1

14.7

8.0

2.4

3.0

2

2025

AAL

American Airlines Group Inc. Common Stock

Consumer Discretionary

Air Freight/Delivery Services

United States

7.325392e+09

NaN

23.8

9.6

11.3

2.9

2.0

3

2025

AAMI

Acadian Asset Management Inc. Common Stock

Finance

Investment Managers

United Kingdom

9.987823e+08

2014.0

31.3

NaN

NaN

NaN

NaN

4

2025

AAON

AAON Inc. Common Stock

Industrials

Industrial Machinery/Components

United States

6.547366e+09

NaN

21.5

NaN

NaN

NaN

NaN

...

...

...

...

...

...

...

...

...

...

...

...

...

...

3130

2025

ZUMZ

Zumiez Inc. Common Stock

Consumer Discretionary

Clothing/Shoe/Accessory Stores

United States

2.929444e+08

2005.0

15.1

NaN

NaN

NaN

1.0

3131

2025

ZVIA

Zevia PBC Class A Common Stock

Consumer Staples

Beverages (Production/Distribution)

United States

1.565735e+08

2021.0

32.9

NaN

NaN

NaN

NaN

3132

2025

ZVRA

Zevra Therapeutics Inc. Common Stock

Health Care

Biotechnology: Pharmaceutical Preparations

United States

4.307623e+08

NaN

34.6

NaN

NaN

NaN

NaN

3133

2025

ZWS

Zurn Elkay Water Solutions Corporation Common ...

Industrials

Industrial Machinery/Components

United States

5.741099e+09

2012.0

14.3

8.3

2.8

3.3

NaN

3134

2025

ZYME

Zymeworks Inc. Common Stock

Health Care

Biotechnology: Pharmaceutical Preparations

United States

8.704068e+08

NaN

29.0

NaN

NaN

NaN

NaN

3135 rows × 13 columns

Stock Data

stocks

Symbol

Name

Date

Open

High

Low

Close

Adj. Close

Volume

Dividend

0

A

Agilent Technologies Inc. Common Stock

2025-03-28

119.21

119.66

116.36

116.69

116.44

1772900.0

NaN

1

A

Agilent Technologies Inc. Common Stock

2025-03-27

120.00

120.33

118.73

118.97

118.72

2075700.0

NaN

2

A

Agilent Technologies Inc. Common Stock

2025-03-26

120.72

121.14

119.05

119.90

119.65

2652900.0

NaN

3

A

Agilent Technologies Inc. Common Stock

2025-03-25

122.60

123.04

119.76

120.51

120.25

1605900.0

NaN

4

A

Agilent Technologies Inc. Common Stock

2025-03-24

121.88

124.43

120.89

121.97

121.71

1557400.0

NaN

...

...

...

...

...

...

...

...

...

...

...

194370

ZTS

Zoetis Inc. Class A Common Stock

2024-01-08

194.53

196.28

192.67

196.15

192.99

1610600.0

NaN

194371

ZTS

Zoetis Inc. Class A Common Stock

2024-01-05

193.07

195.94

193.07

194.85

191.71

1088200.0

NaN

194372

ZTS

Zoetis Inc. Class A Common Stock

2024-01-04

192.85

194.93

192.01

194.04

190.91

1851900.0

NaN

194373

ZTS

Zoetis Inc. Class A Common Stock

2024-01-03

195.92

195.95

192.80

192.93

189.82

1493000.0

NaN

194374

ZTS

Zoetis Inc. Class A Common Stock

2024-01-02

195.79

197.95

195.05

196.57

193.40

1642300.0

NaN

194375 rows × 10 columns

Data Exploration

How concerned are companies with reducing their ESG risk?

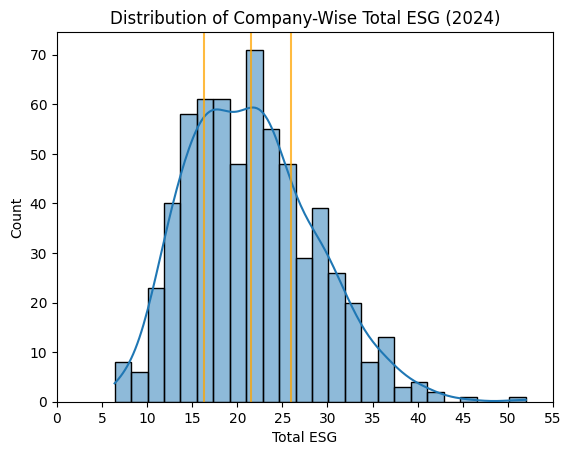

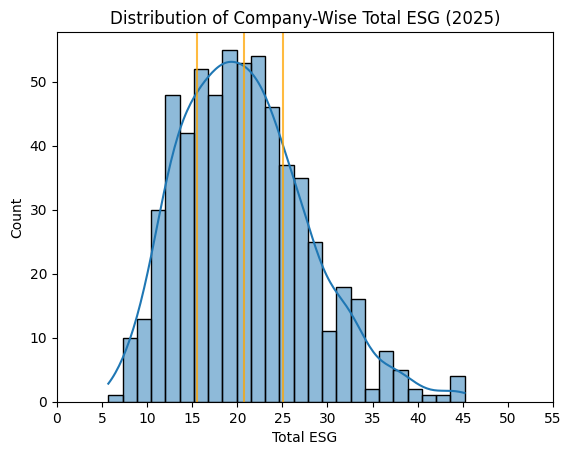

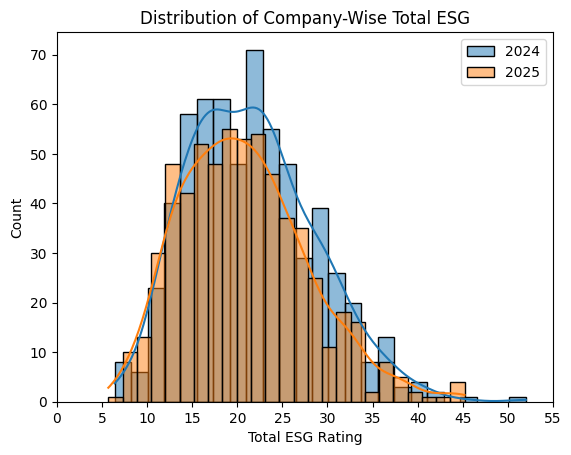

To begin, let’s compare the distribution of Total ESG ratings from the common companies between the two available ESG-related data frames, along with being split by Year:

( sns.histplot(data=esg_2024, x ='total_esg', kde =True, bins =25) .set(xlabel="Total ESG", ylabel="Count", title="Distribution of Company-Wise Total ESG (2024)"))for l in [esg_2024['total_esg'].quantile(0.25), esg_2024['total_esg'].mean() , esg_2024['total_esg'].quantile(0.75)]: plt.axvline(x = l, alpha =0.75, color ='orange')plt.xticks(ticks=[0,5,10,15,20,25,30,35,40,45,50,55])plt.show()

( sns.histplot(data=esg_common_2025, x ='total_esg', kde =True, bins =25) .set(xlabel="Total ESG", ylabel="Count", title="Distribution of Company-Wise Total ESG (2025)"))for l in [esg_common_2025['total_esg'].quantile(0.25), esg_common_2025['total_esg'].mean() , esg_common_2025['total_esg'].quantile(0.75)]: plt.axvline(x = l, alpha =0.75, color ='orange')plt.xticks(ticks=[0,5,10,15,20,25,30,35,40,45,50,55])plt.show()

sns.histplot(data = esg_2024[~esg_2024['total_esg'].isna()], x ='total_esg', kde=True, label ='2024', bins =25),sns.histplot(data = esg_common_2025[~esg_common_2025['total_esg'].isna()], x ='total_esg', kde=True, label ='2025', bins =25)plt.title("Distribution of Company-Wise Total ESG")plt.xlabel("Total ESG Rating")plt.ylabel("Count")plt.xticks(ticks=[0,5,10,15,20,25,30,35,40,45,50,55])plt.legend()plt.show()

From this, it can be observed that there hasn’t been a total ESG shift in favor of a higher/lower average. However, from 2024 to 2025 the distribution of ESG ratings has normalized slightly, dispersing the higher concentration of values surrounding the mean in 2024 more towards the ends of the distribution that reflects movement towards a lower risk overall, though it isn’t significant.

To get a better idea of what caused this dispersion, let’s look at the distributions of the individual parts that make up the Total ESG rating:

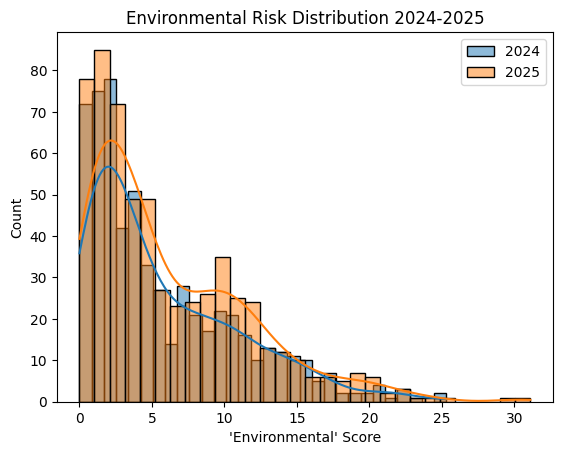

sns.histplot(data = esg_2024[~esg_2024['Environmental'].isna()], x ='Environmental', kde=True, label ='2024', bins =30),sns.histplot(data = esg_common_2025[~esg_common_2025['Environmental'].isna()], x ='Environmental', kde=True, label ='2025', bins =30)plt.title("Environmental Risk Distribution 2024-2025")plt.xlabel("'Environmental' Score")plt.ylabel("Count")plt.legend()plt.show()

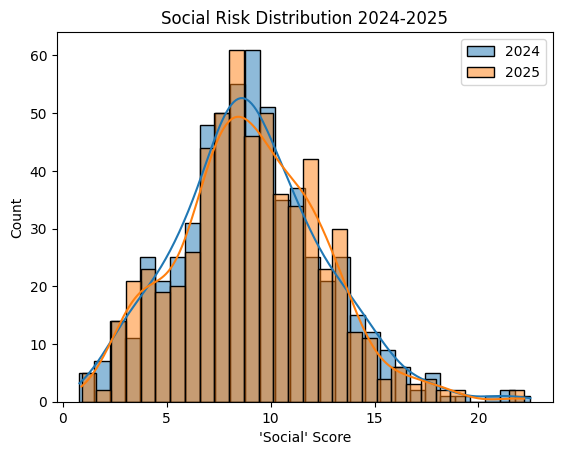

sns.histplot(data = esg_2024[~esg_2024['Social'].isna()], x ='Social', kde=True, label ='2024', bins =30),sns.histplot(data = esg_common_2025[~esg_common_2025['Social'].isna()], x ='Social', kde=True, label ='2025', bins =30)plt.title("Social Risk Distribution 2024-2025")plt.xlabel("'Social' Score")plt.ylabel("Count")plt.legend()plt.show()

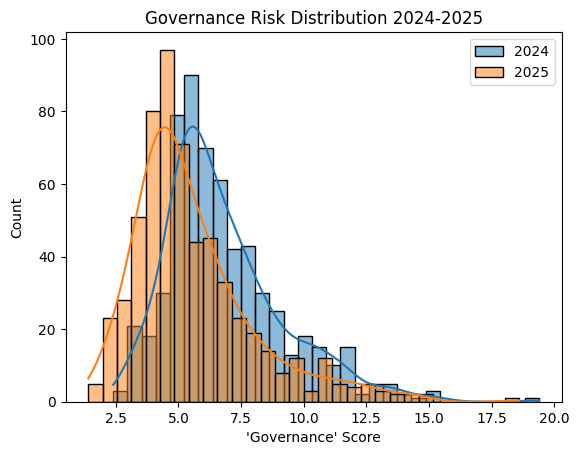

sns.histplot(data = esg_2024[~esg_2024['Governance'].isna()], x ='Governance', kde=True, label ='2024', bins =30),sns.histplot(data = esg_common_2025[~esg_common_2025['Governance'].isna()], x ='Governance', kde=True, label ='2025', bins =30)plt.title("Governance Risk Distribution 2024-2025")plt.xlabel("'Governance' Score")plt.ylabel("Count")plt.legend()plt.show()

Governance is the most adjusted attribute, with there being a real shift in the distribution itself by ~1.25 points in favor of a lower risk, rather than the values being merely redistributed. This tells us that companies have generally been making efforts to refine/redefine their structures, public transparency, and/or stockholder rights.

This is likely due to the 2024 amendment to the ESG by Morningstar to incorporate issues relating to material usage (such as water or raw materials) as a contributor to a lacking corporate governance structure, urging companies to find ways to limit material waste in addition to its existing effect in reducing Environmental risk as well.

Looking at the Environmental distribution, though, we see that this combined effect isn’t received in the same way, with the amount of companies within the low/medium ranks increasing rather than the average decreasing in the same way as Governance did.

One explanation for this could be that there was a reallocation of weights for waste management between the two ratings when the 2024 update occurred, causing the Environmental rating to increase while not being a drastic change as a result of waste management already being a factor, albeit possibly weighted less heavily. For Governance, the waste management parameter was a new addition, so the change would have ended up being more fundamental.

Which Sectors / Industries Typically have the Highest ESG Ratings?

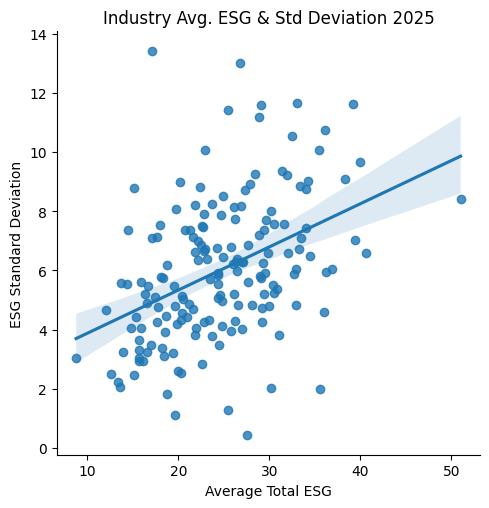

# which industries typically have the highest ESG ratings?mean_esg_2025 = ( esg_2025 .groupby(['Sector', 'Industry']) .agg(esg_mean = ('total_esg', 'mean'), esg_std = ('total_esg', 'std')) .dropna() .reset_index())mean_esg_2025.sort_values('esg_mean', ascending=False)

Sector

Industry

esg_mean

esg_std

65

Energy

Coal Mining

51.025000

8.421698

115

Industrials

Farming/Seeds/Milling

40.575000

6.584515

1

Basic Materials

Metal Mining

39.956250

9.653046

68

Energy

Integrated oil Companies

39.407143

7.042996

70

Energy

Oil & Gas Production

39.156250

11.617241

...

...

...

...

...

12

Consumer Discretionary

Books

13.550000

2.050610

36

Consumer Discretionary

Motor Vehicles

13.425000

2.227667

38

Consumer Discretionary

Newspapers/Magazines

12.600000

2.501999

46

Consumer Discretionary

Publishing

12.100000

4.667333

39

Consumer Discretionary

Office Equipment/Supplies/Services

8.775000

3.031364

166 rows × 4 columns

# Relationship between mean esg and mean esg std deviation; higher mean = higher variancesns.lmplot(data = mean_esg_2025, x ='esg_mean', y ='esg_std')plt.title("Industry Avg. ESG & Std Deviation 2025")plt.xlabel("Average Total ESG")plt.ylabel("ESG Standard Deviation")plt.show()

The prevailing observation here is that there is a strong positive correlation between average ESG and standard deviation. This implies that as ESG ratings become larger, the range between ratings becomes wider in turn, additionally showing that higher ratings among industry peers are less likely to stick as the norm.

More industries/companies are coming to the consensus that a lower ESG score is in their best interests, but is this a financial interest or a public relations interest?

Do ESG Scores Affect Stock Price?

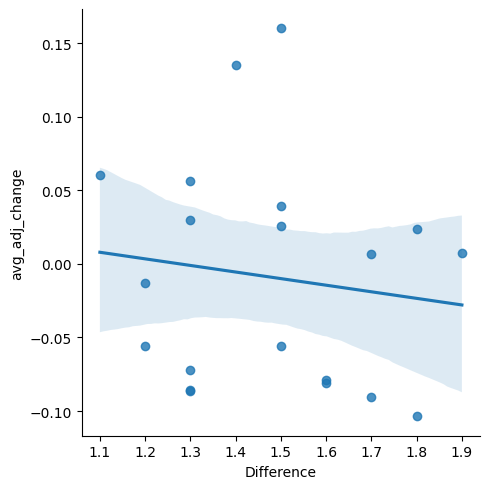

To attempt to answer this question, a possible method could be to plot the relationship between a company’s change in ESG rating and its average stock price. However, this could cause outliers during visualization, beacuse some stocks are valued much higher than others. Instead, I decided to compare the difference in ESG to the average % change of the Adjusted Closing price of a company’s stock, that way the change is more normalized.

Taking a small random sample from the companies with significant differences in ESG scores, we can start to narrow down the nature of this relationship.

def rand_sample(n, start, end, seed): random.seed(seed)return random.sample(range(start, end), n)# Examplerand_sample(15, 100, 300, 10)# A sample of 15 numbers from 100-300, with a set seed of '10'

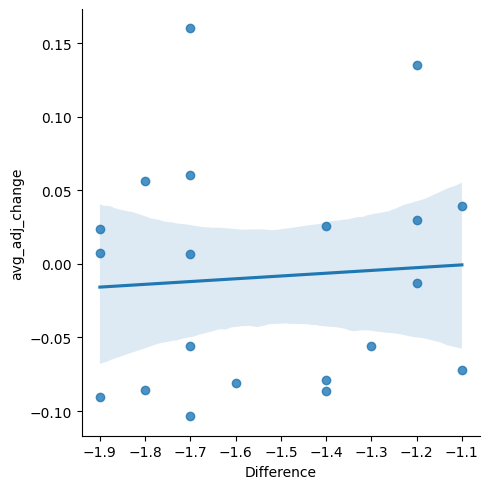

esg_diff_pos['avg_adj_change'] = ( stocks[stocks['Symbol'].isin(esg_diff_pos['Symbol'])] .groupby('Symbol')['adj_pct_change'] .agg('mean') .reset_index(drop=True))sns.lmplot(data = esg_diff_pos, x ='Difference', y ='avg_adj_change')

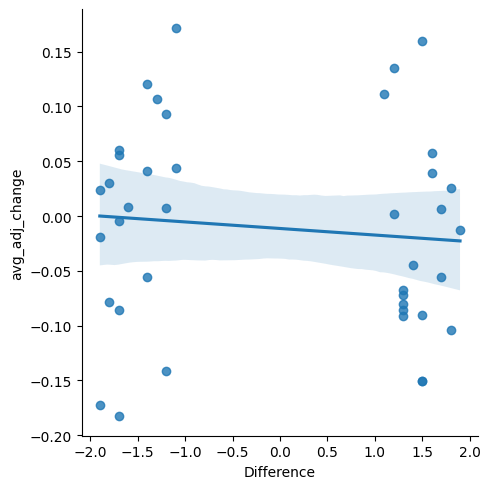

esg_diff_neg['avg_adj_change'] = ( stocks[stocks['Symbol'].isin(esg_diff_pos['Symbol'])] .groupby('Symbol')['adj_pct_change'] .agg('mean') .reset_index(drop=True))sns.lmplot(data = esg_diff_neg, x ='Difference', y ='avg_adj_change')

It appears that there is a trend with there being a large degree of uncertainty for both visualization’s best fit line, which is indicative of there not being a clear relationship between changes in ESG rating and changes in adjusted closing stock price. The two plots reflect two completely different relationships, one where an increase in ESG correlates to negative changes to stock price, and one where an increase in ESG correlates to a more positive change.

Even with a combination of these data points, the lack of a definitive relationship is clear, indicated by the near horizontal regression line:

esg_diff_comb = pd.concat([esg_diff_pos, esg_diff_neg]).reset_index(drop=True)esg_diff_comb['avg_adj_change'] = ( stocks[stocks['Symbol'].isin(esg_diff_comb['Symbol'])] .groupby('Symbol')['adj_pct_change'] .agg('mean') .reset_index(drop=True))sns.lmplot(data = esg_diff_comb, x ='Difference', y ='avg_adj_change')

print("Despite this,", esg_diff.query("Difference < 0")['Difference'].shape[0] / esg_diff['Difference'].shape[0] *100, "percent of ESG ratings have lowered between 2024 and 2025.")

Despite this, 63.2 percent of ESG ratings have lowered between 2024 and 2025.

Conclusion

In conclusion, although ESG score metrics impact the public outlook of a company, and are not uncommonly considered during consumer investment decisions, they doesn’t seem to retain much usefulness when it comes to a company’s financial gain/loss from stocks.

A company’s incentive to decrease their ESG rating likely comes from either the desire to be looked upon favorably in comparison to their peers or from the pressures of having a standardized metric of sustainability that they could possibly be held accountable for. Regardless of the lack of a clear relationship, companies are vying for lower ESG ratings as time goes on, improving their corporate structures and endeavoring to make environmentally sustainable decisions, the importance of which cannot be understated.